Search

Tax Problems Following a Divorce or Marital Problems? Innocent Spouse Relief May Be an Option

Many married couples find it advantageous to file a joint tax return rather than filing separately. This comes as no surprise as the federal government has built a number of tax advantages for married couples filing jointly into the tax code. These benefits include:

- Depending income distribution, a lower rate of taxation than they would face filing separately.

- Increased limits for charitable deductions

- IRA and retirement account benefits

- Estate protection

- Reduced tax administration expenses

However there are also drawbacks to filing jointly with your spouse – especially so if the relationship hits a rough patch or ends in divorce. This is because by filing jointly, you subject yourself to joint and individual liability for everything that appears on the tax return. In other words, absent an exception or relief both members of the couple are liable for everything that appears on the tax form regardless of who prepared it. If your spouse or former spouse made mistakes on the jointly filed taxes or took overly aggressive positions you could find yourself liable for underpayments, fines and penalties.

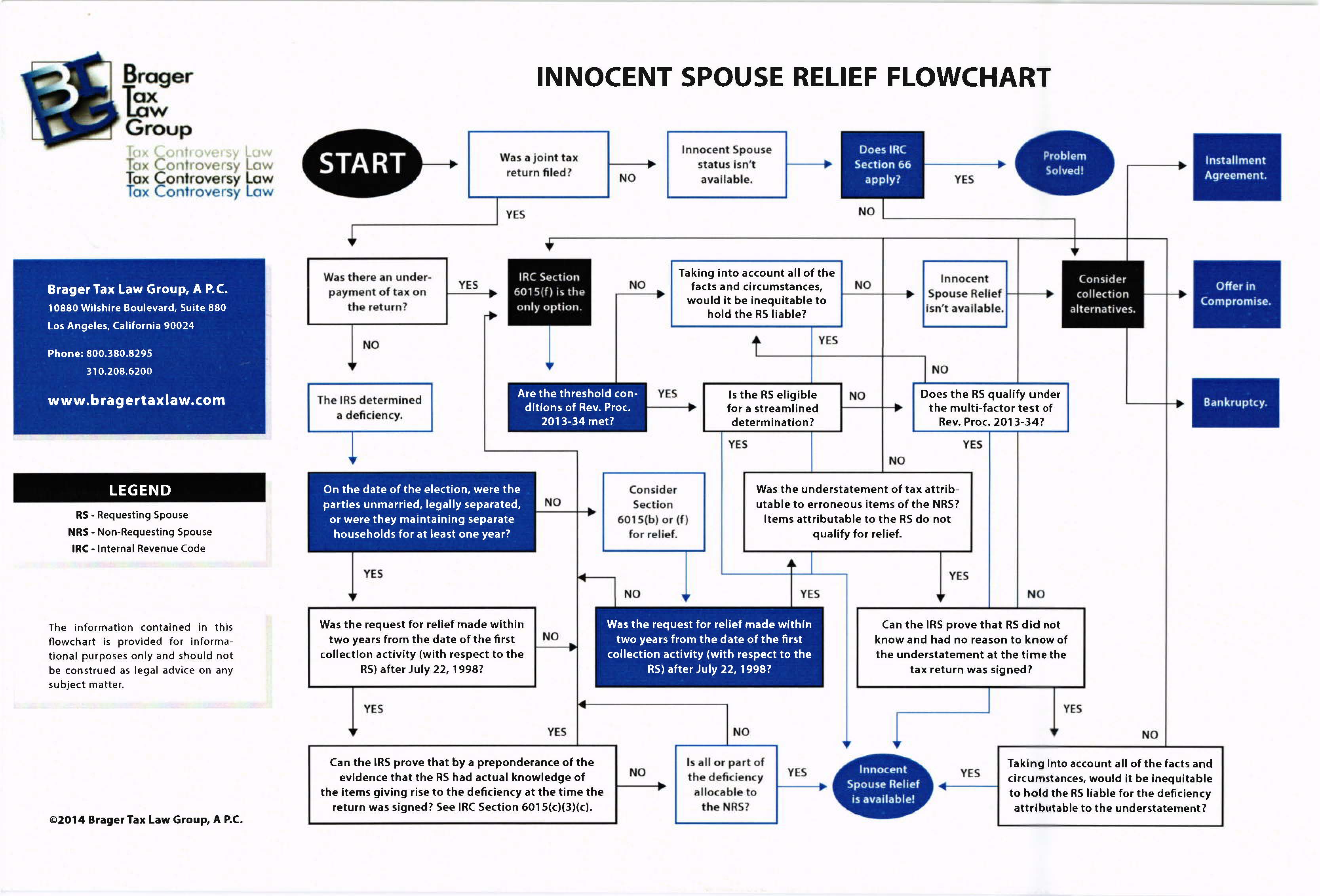

When is applying for innocent spouse relief appropriate?

The most common instance where issues of innocent spouse relief may come into play is where a couple is headed down the path to a divorce or has already divorced. Often, one of the partners in the marriage was responsible for handling the taxes and the other partner may have only had a limited role in preparing or overseeing the taxes. In the most extreme case, the other spouse may do little more than simply sign off on the return while trusting that his or her partner prepared the taxes thoroughly and accurately.

At some point, the spouse who participated only minimally in the tax preparation process may suspect that his or her spouse may have understated income, overstated deductions or exemptions, or otherwise violated the tax code or committed tax crimes. The innocent taxpayer does not want to remain liable for these outstanding tax debts and penalties because he or she did not create them or cause them. It may be appropriate for a spouse in a spouse in this or a similar position to file for innocent spouse relief.

To apply for innocent spouse relief a taxpayer must file Form 8857 with the IRS. The form must detail and explain why the taxpayer believes that he or she is entitled to such relief. By filing Form 8857 you are asking the IRS to establish a separate tax liability for you that is separate and apart from that of your current or soon-to-be former spouse, or ex-spouse. On the form you must provide information regarding your role in the tax preparation process, whether you were aware of the income, if you had reason to know about the inaccurate statements on the tax form. Depending upon the type of tax relief requested, the filing taxpayer may be required to prove that it would be unfair to hold him or her liable for the tax liability. Whether something is fair or unfair can be highly subjective, but the IRS has provided criteria to help in making this determination. Elements the IRS will examine to determine whether it would be fair to impose the tax against the spouse filing for relief include:

- The nature of the erroneous item or items on the tax filing

- The value of the erroneous item or items relative to the remaining items on the tax return

- The level of participation by the filing taxpayer in the mistake or scheme

- The filing spouse’s experience in business dealings

- The filing spouse’s educational history

- The financial circumstances of each spouse

- Whether the filing party failed to ask reasonable questions about the return prior to authentication.

- Is the understatement part of a recurring pattern or an isolated incident?

All of these items will be considered as part of the inquiry as to whether it would be fair to impose the tax liability and decline to provide relief. However other additional requirements apply. For instance, an application for relief must, generally, be filed within two years of the first collection action taken by the IRS, but there are exceptions.

Tax issues after a divorce?

While the standards to be granted innocent spouse status are high, taxpayers are entitled to appeal an IRS determination that is not in their favor to the United States Tax Court. The Brager Tax Law Group can assist you in filing either an initial application for innocent spouse status or in preparing an appeal. By securing this status you may be able to not only resolve the current debt, but will also bring most enforced collection activity to a halt. However, the extent of the relief even if granted can vary based upon the type of relief granted, the terms of the divorce decree, and even the timing of the divorce, and the division of assets. For a confidential tax consultation call our firm at 800-380-TAX-LITIGATOR today or contact us online.